Bank Manager Refused to Cash a Black Man’s Check 3 Times — His Balance Made Her Drop the Pen

She smirked, slid his check back across the counter, and said ‘come back with proper ID’—three times. Then he calmly pulled out his phone, showed her his balance, and watched her hand tremble so hard she couldn’t sign the withdrawal slip. The bank branch went silent. The regional manager was called. And by noon, she was cleaning out her own desk.

Get this roach out of my bank.

Claire Dawson said it in the middle of the lobby.

Now, hands on hips, pearl earrings. Not a whisper, a command.

Third time this week. Same bank, same check, same answer.

This is my money. My check.

A quarter million from you. Who’d you steal it from?

I’m asking you to do your job.

Stray dogs don’t get served at this counter. Not today. Not ever.

Six customers watched. Nobody moved.

The security guard stepped closer.

He folded the check, slid it into his pocket, and said:

I gave you three chances.

Then he walked out.

What Claire didn’t know—what nobody in that lobby knew—was that the man she just called a stray dog was about to come back. And this time around… buckle up.

To understand what just happened, we have to go back to where it all started.

Three days earlier. Monday morning. 6:15 a.m.

A quiet suburb in Ridgewood, New Jersey.

Aaron Mitchell woke up the same way he always did. No alarm. Just sunlight through thin curtains and the sound of his dog scratching at the bedroom door.

He made coffee in a kitchen that smelled like old wood and fresh grounds. Nothing fancy. A drip machine from Target. A chipped mug with no logo.

He stood by the window, watching the neighborhood wake up.

From the outside, nothing about Aaron screamed money. A small one-story house. A garden with tomatoes. A ten-year-old SUV with a scratched bumper and faded paint.

His neighbors knew him as the quiet guy who moved in six months ago. Friendly. Polite. Unremarkable.

That was the point.

What nobody in Ridgewood knew was that Aaron Mitchell owned Mitchell Capital Holdings, a private equity firm managing over $800 million in assets.

He built it from nothing. No inheritance. No family money. A foster kid who aged out of the system at 18 with $200 and a library card.

But he never wore his wealth. No Rolex. No designer shoes. Just his late mother’s Timex on his wrist—the only thing she left him.

He wore it every day. Not because it was valuable. Because she was.

That morning, he put on a clean pair of jeans and a plain navy shirt.

He picked up a manila envelope from the counter. Inside: a cashier’s check for $250,000.

A routine transfer between his own accounts.

He drove to First Union Savings Bank in Ridgewood.

Polished marble floors. Brass handles. Soft jazz in the air. The kind of place that felt like it only belonged to certain people.

Aaron walked in at 10:15 a.m.

A few heads turned. Then turned away. Measuring him in a single glance.

He approached the counter.

A young teller, Nina Vasquez, greeted him with a professional smile.

He slid the check across the counter along with every piece of identification possible.

“I’d like to deposit this into my checking account, please.”

She scanned it. Everything checked out. Routine transaction. Two minutes.

Then a voice came from behind her.

“Hold that transaction.”

Claire Dawson, branch manager. Late 40s. Blonde hair tight. Cream blazer. Pearl earrings.

She looked at the check. Then at Aaron. Slowly. Head to toe.

She took the check into her office.

Five minutes turned into twenty.

Customers who arrived after him were served and left. No delays. No questions.

When Claire returned, her smile was thin.

“I’m sorry, sir. This check cannot be verified at this time. You’ll need to come back tomorrow with additional identification.”

Aaron looked at the stack of ID on the counter.

“What additional identification?”

“We just need to be thorough with amounts like this.”

She never made the verification call. The phone stayed untouched. Aaron saw it.

He left without another word.

That evening, he sat in his driveway with the engine off. The envelope on the passenger seat.

Not anger. Not shock. Just exhaustion.

He had felt it before—being measured before being known.

But a bank was different. A bank is supposed to work for you.

Still, he didn’t call anyone.

He could have ended it with one phone call to his company. One call. And everything would have changed for Claire Dawson.

But he didn’t.

He wanted to see what would happen if he came back as just himself.

Wednesday morning. 9:45 a.m.

Same check. Same man. Same calm voice.

Nina recognized him immediately.

“Good morning, Mr. Mitchell.”

He slid the check again.

This time Nina hesitated, then went to Claire.

Through the glass, Aaron watched Claire dismiss her with a wave.

Extended review. Five to ten business days.

A cashier’s check from a top bank—delayed for no reason that made sense.

Aaron asked to speak directly with Claire.

“She’s in a meeting.”

She wasn’t. She was eating salad at her desk.

Their eyes met through the glass. Claire looked away.

Aaron left again.

That night, Nina couldn’t sleep.

Friday morning. 10:00 a.m.

Aaron returned a third time.

This time, something in him had changed. Not his clothes. His posture. His decision.

He had spoken to his attorney the night before. Terrence Moore.

Terrence offered to come with him.

Aaron refused.

“Not yet.”

He walked into the bank alone.

Claire saw him immediately.

“I’ve already explained—your check is under review. Stop coming in here every other day.”

Her voice was loud. Deliberate. Public.

Aaron placed the envelope on the counter.

“I’d like to deposit my check.”

Then, calmly:

“I’ve given you every form of identification. I’ve been patient. I’m asking you to do your job.”

Claire stepped closer.

“I don’t trust people who show up three times in a week in clothes that cost less than my lunch.”

The words hit the room. Nobody moved.

Aaron didn’t react.

“I’d like to see the written policy that allows you to hold a verified cashier’s check for ten business days.”

“I don’t have to show you anything.”

That was enough.

She signaled the security guard.

The guard stepped in beside Aaron. Close. Intentional.

The message was clear. Threat, not customer.

Claire crossed her arms.

“If you continue being disruptive, I will have you escorted out.”

Aaron looked around the room. Six people watching. Nobody speaking.

He picked up the envelope slowly.

“You’re right. We’re done here.”

He leaned in slightly.

“I gave you three chances.”

“Three. And all three times, you chose this.”

Something flickered in Claire’s expression—uncertainty, just for a second.

Aaron turned and walked out.

The marble floor echoed under his steps.

The guard stepped aside.

The door opened.

And the morning air hit him—cool, sharp, real.

Terrence was leaning against the car, arms folded, watching through his sunglasses.

“How’d it go?”

Aaron opened the passenger door, sat down, and closed his eyes for three seconds.

“She called the security guard on me.”

Terrence pulled off his sunglasses. His jaw tightened.

“Then we’re done being polite.”

Aaron looked at him.

“We’re done being polite.”

Terrence didn’t go home. He went straight to Aaron’s kitchen table, laptop open, legal pad out, three pens lined up like bullets.

Aaron made coffee—two cups, black, no sugar. He set one in front of Terrence and sat across from him.

For a long moment, neither of them spoke.

The house was quiet. The dog snored on the couch. The coffee maker ticked as it cooled.

Terrence broke the silence.

“Tell me everything from the first visit. Don’t leave out a single word.”

Aaron told him everything. All three visits. Every look. Every word. The salad. The security guard. The cologne. Claire’s smile—tight, controlled, porcelain.

Terrence wrote it all down. Dates. Times. Names.

He circled three things twice:

No verification call made. No fraud report filed. No written policy produced.

“She’s got nothing,” Terrence said. “No legitimate reason. Not one.”

“I know.”

“So what do you want to do?”

Aaron looked at the envelope on the counter. The check inside was still crisp, still valid, still his.

“I don’t just want my check cashed,” Aaron said. “I want to know how many other people she did this to. And who let her.”

That was the moment everything shifted.

This was no longer about a check. It was about a pattern.

Terrence made the first call that afternoon—not to a lawyer, not to a reporter, but to the regional headquarters of First Union Savings Bank.

He stayed calm. Professional.

He identified himself as legal counsel for a client who had experienced repeated service denials at the Ridgewood branch. He requested the deputy regional director.

He was transferred three times, held for twenty-two minutes, then transferred again.

Finally, compliance picked up.

Branch managers have discretionary authority over flagged transactions, they said. The bank supports Ms. Dawson’s judgment.

Terrence asked if they had reviewed the specifics.

A pause.

“I’m not authorized to discuss individual customer interactions.”

He hung up. Looked at Aaron.

“They’re backing her.”

Aaron nodded slowly.

“For now.”

That night, Terrence dug.

Public records. Consumer complaint databases. Regulatory filings. CFPB reports.

He wasn’t looking for drama. He was looking for patterns.

And he found one.

Six formal complaints in twenty-four months against the Ridgewood branch of First Union Savings Bank.

All six from Black or Latino customers.

All six describing the same pattern: delayed transactions, unexplained holds, extended “reviews” that never ended.

One stood out.

A small business owner named Gerald Davis had tried to deposit a $38,000 business check. Legitimate. Verified.

Claire held it for fifteen days.

No fraud report. No explanation. No resolution.

On day sixteen, he closed his account.

His words in the complaint:

“I felt like a criminal for trying to deposit my own money.”

The case was marked “resolved internally.” No investigation. No consequence.

Terrence spread the papers across the table.

Six complaints. Six people of color. Six ignored cases.

Aaron read them in silence.

When he finally spoke, his voice was steady—but heavy.

“She’s been doing this for years.”

“And they let her,” Terrence said.

That afternoon, Terrence called again. Then again. Then he escalated.

Consumer Financial Protection Bureau complaint. Formal filing. Detailed documentation. Every visit, every word, every policy failure.

Then a second letter—this one sent directly to corporate legal at First Union’s Manhattan headquarters.

Eleven pages. Precise. Clinical. Damning.

It outlined Aaron’s three visits, the lack of verification, the absence of fraud procedure, and the pattern of six prior complaints.

The final paragraph was simple:

“My client is prepared to pursue all available remedies—regulatory, civil, and public—if this matter is not addressed immediately and transparently.”

Terrence also called a civil rights law firm on the East Coast.

Forty-five minutes later, they had co-counsel and a strategy.

This was no longer a complaint. It was a case.

While Aaron and Terrence built their case, change was already starting elsewhere.

Nina Vasquez couldn’t stop thinking about Friday.

The words. The silence. The guard stepping forward.

“Stray dogs don’t get served at this counter.”

She had seen Claire do smaller versions of it before. Not as loud. Not as direct. But the pattern was there.

And she had stayed quiet.

Until now.

That night, Nina opened her phone. She had recorded part of the encounter—ninety seconds of shaky footage from under the counter.

Claire’s voice cut through the clip. Clear. Cold.

The silence afterward. The jazz still playing. The guard’s footsteps.

Nina watched it three times.

Then she called a friend who worked at a regional news outlet.

“I need to talk to you,” she said. “Not as a friend. As a journalist.”

She didn’t send the video yet. But the line had been crossed.

Monday morning, Terrence filed a CFPB complaint.

Same day, he sent the corporate legal team an eleven-page letter.

Same day, he called a major civil rights firm.

And in Manhattan, First Union’s legal department finally took notice.

The file was no longer local.

It was escalation.

Meanwhile, Claire sat in the break room, laughing over a turkey wrap.

She told her coworkers she had caught a suspicious transaction.

“You learn to read people,” she said. “Twenty years in banking.”

That same morning, regional leadership called her.

Not to punish her.

To prepare her.

“Write a justification for the holds,” they said. “Dates. Reasons. Be thorough.”

She thought that meant she was safe.

She was wrong.

Because Monday morning, a different door opened.

Sandra Ellis, senior vice president of compliance, arrived at the Ridgewood branch with internal audit.

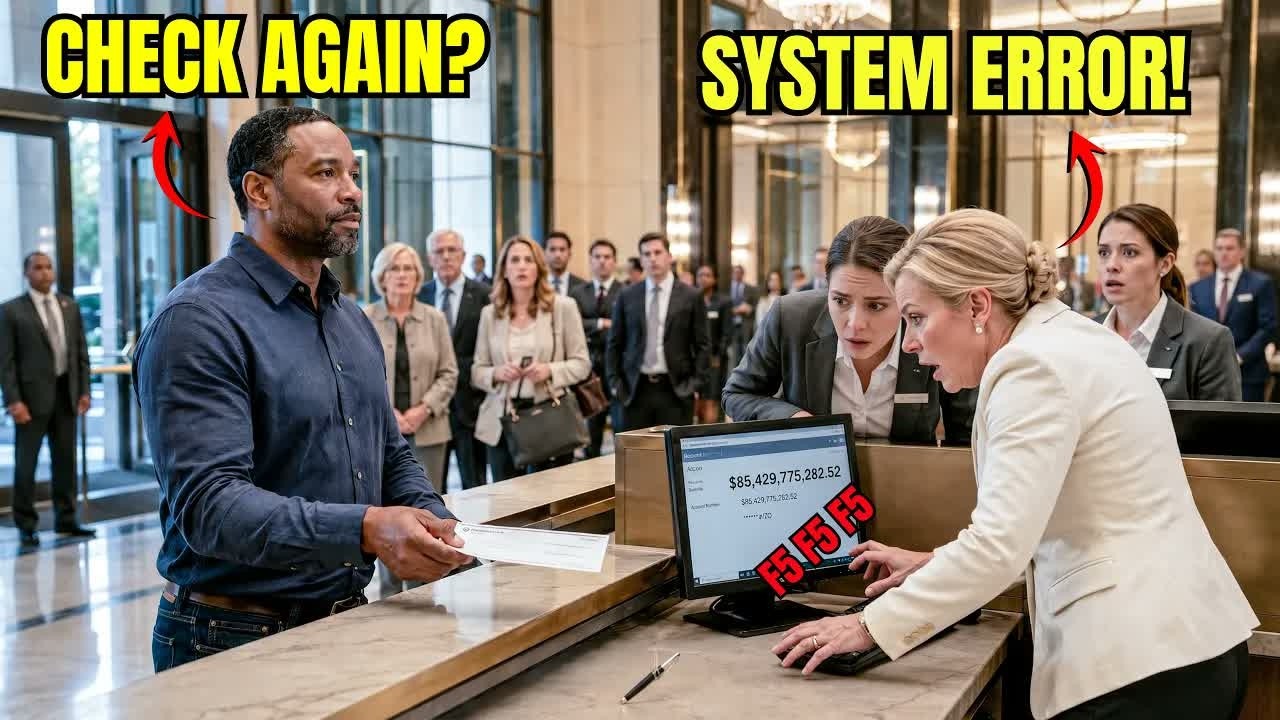

And when Claire pulled up Aaron Mitchell’s profile, her entire world stopped.

Checking account: $4,200.

Then came the rest.

Private wealth portfolio. Trust accounts. Brokerage holdings.

Total value: $412 million.

The cashier’s check she blocked wasn’t suspicious.

It was internal.

Money moving between accounts inside her own institution.

She had not stopped fraud.

She had stopped a client.

A very large one.

Sandra didn’t raise her voice. She didn’t need to.

“You refused to process an internal transfer for one of this institution’s largest clients,” she said. “Three times.”

Claire tried to speak. Nothing came out clean.

“I used my judgment,” she finally said. “Twenty years of experience—”

“Did you verify it?”

Silence.

“Did you contact wealth management?”

Silence again.

Sandra opened the folder.

Six complaints. Six customers. Six ignored patterns.

“This isn’t judgment,” she said quietly.

“This is exposure.”

Aaron stepped forward. He didn’t raise his voice. He didn’t need to.

“I opened that checking account on purpose three weeks ago because I’d heard the complaints. I’d read the stories, and I wanted to see for myself.”

He paused. Let it land.

“I walked in here three times dressed like this. No title, no entourage—just a man with a valid check. And three times you decided I wasn’t worth your time.”

Claire’s eyes were wet—not from remorse, but from the sudden, crushing realization of what she had done and who she had done it to.

“I’m withdrawing every dollar from this institution today. All 412 million. My attorneys will handle the rest.”

The words hit the room like a wave.

Sandra Ellis and Raymond Torres exchanged a glance—the kind that says this is going to be very, very bad.

Claire opened her mouth. Nothing came out.

Aaron turned toward the door. Terrence followed.

At the threshold, Aaron stopped. He didn’t look back.

“You called me a stray dog, Miss Dawson, in front of everyone in this lobby. I want you to remember that—because that stray dog just cost you everything.”

The glass door swung shut behind him.

The jazz kept playing. The brass fixtures still gleamed. But something in that lobby had cracked open—and it was never going back together.

Claire didn’t move for a full minute after Aaron left. She sat at the terminal, staring at the screen. Her dropped pen still lay on the desk. The number glowed back at her.

$412 million.

$412 million.

The man she called a roach. The man she called a stray dog.

Sandra Ellis broke the silence.

“Miss Dawson, please step into your office now.”

Claire stood. Her legs were unsteady. She walked into the glass office—the same office where she had eaten her salad while Aaron waited. The same office where she had waved Nina away like a fly. Now it felt like a cage.

Sandra closed the door. Raymond Torres stood outside, already on his phone.

“Miss Dawson, effective immediately, you are placed on administrative leave pending a full internal investigation.”

Claire’s voice cracked.

“Sandra, please. This was a misunderstanding. I was protecting the bank. I was doing my job.”

“Your job was to serve the customer. You refused three times. No documentation. No verification. No fraud report. Nothing.”

“I can fix this. Let me call him. Let me process the check right now—I’ll do it myself.”

“It’s too late for that.”

Sandra held out her hand.

“Your access badge, please.”

Claire stared at the open palm. Her fingers went to her blazer. The badge she had worn every day for six years. The badge that made her the most powerful person in that lobby.

She unclipped it and placed it in Sandra’s hand.

No sound.

But it felt like the loudest thing in the room.

“You’ll need to collect your personal belongings. Security will escort you out.”

Twenty minutes later, Claire Dawson walked through the lobby carrying a cardboard box.

Inside: a framed company photo, a mug that said “World’s Best Boss,” a desk calendar, a lint roller. Six years of authority reduced to cardboard weight.

Nina watched from behind the counter. So did the other tellers. So did the customers.

The same security guard who had stood beside Aaron opened the front door for her. He didn’t look at her once.

Claire stepped outside.

The morning air hit her face. The parking lot was bright and ordinary. Birds on the power line. A woman loading groceries. Nobody noticed. Nobody cared. The world kept moving without her in it.

Inside, Raymond Torres was already on the phone with corporate. The number “412 million” had moved up the chain faster than any memo in First Union history.

By noon, Philip Caldwell got the call.

Not a warning. Not a coaching session. A conference call with corporate legal, compliance, and the CEO’s office.

“Phillip, we have a record of a call you made last Monday instructing Ms. Dawson to create retroactive documentation to justify the holds. Is that correct?”

His mouth went dry.

“I—I was advising—”

“You were coaching a branch manager to fabricate a paper trail after a formal complaint. That is obstruction.”

Silence.

“You are placed on administrative leave effective immediately. Do not contact Ms. Dawson. Do not contact the branch. Do not contact Mr. Mitchell or his counsel.”

The line went dead.

By 3:00 p.m., both Claire and Philip were gone—badges deactivated, access revoked, desks emptied.

Terrence received the confirmation at 3:45.

“They want to talk settlement,” the corporate lawyer said. “They want to keep Mr. Mitchell as a client.”

Terrence replied:

“My client’s decision is final.”

Aaron was on his porch when he heard. Dog at his feet. Afternoon sun cutting through the trees.

“Claire’s out. Philip’s out. Corporate is scrambling.”

Aaron was quiet for a moment. He scratched the dog behind the ears.

“Good.”

Then:

“But we’re not done. Not even close.”